The Four Indias of Healthcare

Why "pan-India" is usually a lie, and where the next decade will actually be won.

Most Indian healthcare strategies fail for the same reason: they pretend the country is one market. It isn't. It's four. And once you see them separately, almost every "pan-India" pitch, deck and policy paper looks incomplete.

The problem with "One India"

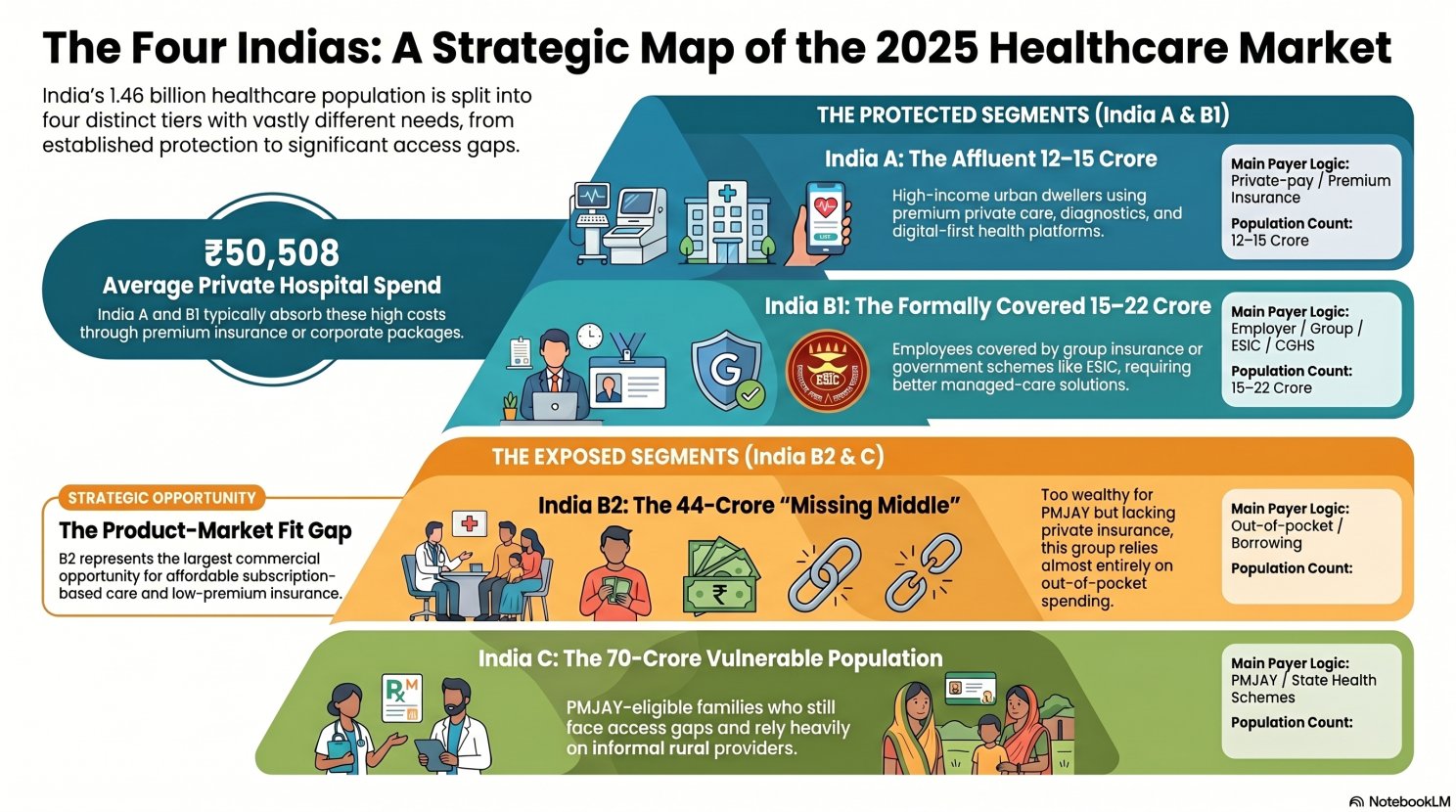

Every healthcare deck opens the same way: 1.4 billion people, 3%+ of GDP on health, a rising middle class, a digital health wave. All true. All useless. Because the average Indian healthcare consumer doesn't exist. The Bangalore IT manager buying a ₹50,000 health check-up and the Bihar farmer borrowing from a moneylender to pay for his wife's hospitalization are not in the same market. They're not even in the same economy. They're in completely different Indias.

There isn't one India. There are four.

Has access

Urban high-income. Employer or private insurance, direct pay if needed. Uses premium hospitals, super-specialists, digital-first platforms. Over-served, but profitable.

Has partial protection

Covered by ESIC, CGHS, corporate group or retail insurance. Cashless access exists, but so do network limits, sub-limits, exclusions and co-pays.

Has willingness to pay but no product

Self-employed farmers, shop owners, gig and informal workers. Not poor enough for PMJAY, not rich enough for private insurance. Pays mostly out-of-pocket. NITI Aayog says they can afford ₹4,000–6,000 per family per year for hospitalisation cover. Nobody is selling it to them.

Has entitlement but poor usability

Bottom half by income: rural poor, casual labour, small tenant farmers. Entitled to PMJAY's ₹5 lakh cover on paper. In practice: cards issued, awareness low, nearest empanelled hospital far away, outpatient not covered.

Four segments. Four completely different failure modes. Four completely different strategies. And yet most healthcare companies try to serve "India" with one operating model. That's why most of them struggle outside the metros.

Three insights this frame surfaces

1. B2 is not poor. B2 has money. This is the biggest misread in Indian healthcare strategy. The missing middle is ~44 crore people who can pay, roughly ₹5,000 a year for OPD and ₹4,000–6,000 a year for family hospitalization cover. Aggregate that and you're looking at an addressable premium pool of ₹2 lakh crore that almost no major insurer is building for. The businesses that define Indian health insurance in 2030 are being designed for B2 right now, and not by the companies currently dominating the IRDAI league tables.

2. B1 is a managed-care problem, not a distribution problem. The formally insured middle already has coverage. What they don't have is a product that works, without six-hour claims calls, ₹75,000 room-rent caps, and pre-existing disease exclusions that surface when the claim is filed. The play here is TPA automation, employer health platforms, chronic care bundles and OPD bolt-ons. Unsexy. Enormous. Almost entirely untouched by the Indian health-tech VC narrative.

3. Commercial strategy and policy strategy separate cleanly. India-C is a public finance problem; expecting a private company to build a profitable primary-care business serving it confuses social infrastructure with commercial opportunity. India-B2 is the opposite, a commercial problem dressed up as a policy problem, solved by entrepreneurs, not ministries. Mixing the two is how strategies get built that are too soft to be commercial and too commercial to be social.

The question every healthcare CEO must answer: not which India you say you serve. Which does your P&L actually serve?

Three questions, in order. First, which India does your business actually serve today, by revenue, not press release? Most "pan-India" claims dissolve into India-A with aspirations. Second, what is your moat in that specific India? Moats don't transfer: brand equity in India-A doesn't win India-B1, and cost discipline in India-B2 doesn't earn loyalty in India-A. Third, if you want the next India, is that a different business? Usually it is: separate brand, P&L, leadership and capital pool.

Three signals that tell you how fast this map is shifting

Watch IRDAI's Bima Sugam rollout: if low-ticket, OPD-inclusive insurance becomes real, B2 unlocks overnight. Watch PMJAY OPD expansion: every credible health economist argues for it, and when it comes, the India-C operating model changes. And watch the next Tata 1mg / PharmEasy / Apollo 24/7 move: whoever cracks tier-3 and below with a scheme-native model owns the decade.

Capital flows to A. Lives concentrate in C. The next decade's winners build for B2 and extend into C.

India's healthcare market is not one market. It is four, with different economics, payers, providers and kinds of failure. Leaders who accept that and choose which India they're building for will compound. Leaders who keep writing "India" on their slides and wondering why the growth numbers only add up in PowerPoint will not.

Sources: NITI Aayog (2021) on the missing middle · IRDAI 2024-25 Annual Report · National Health Accounts FY22 · NSS 75th round (2025) · J-PAL on informal providers · UNFPA 2025 population estimate.