The Orchestration Gap: Why Mid-Tier Indian Hospitals Are Losing

International patients are knocking. Mid-tier hospitals aren't converting. Here's what Tier-1 chains figured out, and what most CEOs are still missing.

The uncomfortable truth

Indian medicine is world-class. For most hospitals, Indian medical tourism is not. Clinical capability is there. Pricing is brutal: 60–90% lower than the US. Wait times are near zero. International inquiries land in mid-tier hospital inboxes every single day, and most of them die before becoming treated patients. This isn't a clinical problem, it's an orchestration problem, and it's why Apollo, Fortis, Manipal, Medanta and Max are quietly walking away with revenue mid-tier hospitals already had access to.

The demand has never been stronger

US healthcare costs are spiraling: family premiums rose 6% in 2025, outpacing wage growth (4%) and inflation (2.7%), and that gap has compounded for over a decade. Elective wait times of six months are routine across the UK, Canada and Europe. India hosted 650,000 international patients in 2024, up from roughly 180,000 in 2020. Medical tourism now drives 7–12% of revenue at major corporate hospitals. The demand is real. The spoils aren't being shared evenly.

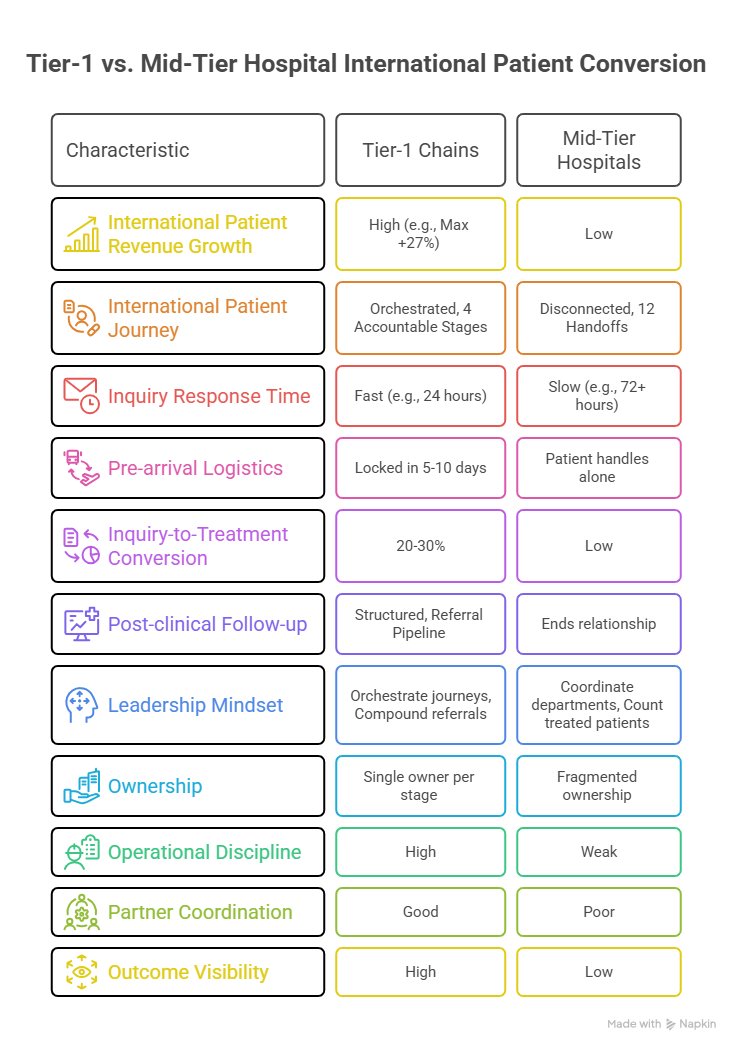

Tier-1 is pulling away

FY24 international patient revenue growth tells the story: Max +27%, Medanta +24%, Fortis +12.2%, Apollo's international revenue rising from 7% to 10% of total in FY25, and Manipal drawing 20–25% of medical-value-travel revenue from West Asia alone. Same demand pool, same inquiries flowing to mid-tier hospitals too, wildly different outcomes. The question every mid-tier CEO should ask: what do they know that we don't?

The diagnosis: a 12-step mess with no owner

The international patient journey isn't one process. It's 12 disconnected handoffs spanning inquiry, estimate, visa, travel, admission, treatment, billing, discharge and follow-up. Each step touches a different team or partner. None of them owns the patient end-to-end. Inquiries sit unanswered for 72+ hours. Cost estimates float between facilitators, doctors and finance with no one owning the number. The patient figures out visas, flights and accommodation alone. Discharge ends the relationship instead of starting the referral pipeline. The patient doesn't experience clinical excellence, they experience anxiety, ambiguity and friction, and they drop off long before they land in India.

The fix: 12 steps become 4 accountable stages

The HFS Operational Playbook collapses the mess into four orchestrated stages, each with a single owner and measurable conversion targets.

Pre-arrival

Capture demand, assess fit, secure commitment. Where most lose 70%+ of inquiries today.

Pre-clinical logistics

Lock visa, travel, accommodation, in-country readiness. Decides if the patient shows up.

Clinical

Coordinated care from arrival to discharge under one accountable owner.

Post-clinical

Structured follow-up that turns one patient into 3–5 referrals. Almost no mid-tier does this well.

Benchmarks to chase: inquiries answered in 24 hours, pre-arrival logistics locked in 5–10 days, 20–30% inquiry-to-treatment conversion, and a measurable referral pipeline from follow-up. Anything less is leakage.

The bigger shift is mental

The hard part isn't the tech stack, it's the leadership mindset. Stop coordinating departments and start orchestrating journeys. Stop counting treated patients and start compounding referrals. Stop optimizing touchpoints and start designing the whole flow. This is a CEO-level mandate. If the CEO isn't driving it, it doesn't happen.

Where this goes wrong

Five risks quietly kill these programs: fragmented ownership with no single accountable owner; standalone tech investments that replace analog fragmentation with digital fragmentation; weak operational discipline with no SLAs, conversion tracking or escalation paths; poor partner coordination across travel, visa and accommodation silos; and no outcome visibility, so conversion can't be measured or improved. Most programs fail on execution discipline, not strategy.

The only question is whether mid-tier hospitals will build the orchestration layer to convert demand into treated patients, or keep watching Tier-1 chains capture the upside on opportunities that landed in their own inbox first.

The demand is showing up. The clinical capability is there. The pricing advantage is structural. The HFS Operational Playbook lays out the full 4-stage operating model, a 12-month transformation timeline, and the conversion benchmarks Tier-1 chains are already hitting. If you're a hospital CEO, COO or IPD leader rebuilding your international strategy in 2026, it's worth 15 focused minutes.