The 1% Problem Every Indian Pharma CEO Is Ignoring

India's pharma market grew 8.1% last year. Only 1.5% came from real demand. Here's why the other 6.6% is a slow-moving crisis.

India's pharmaceutical industry has a 1% problem, and almost no one is talking about it. Most CEOs are still optimizing the wrong number.

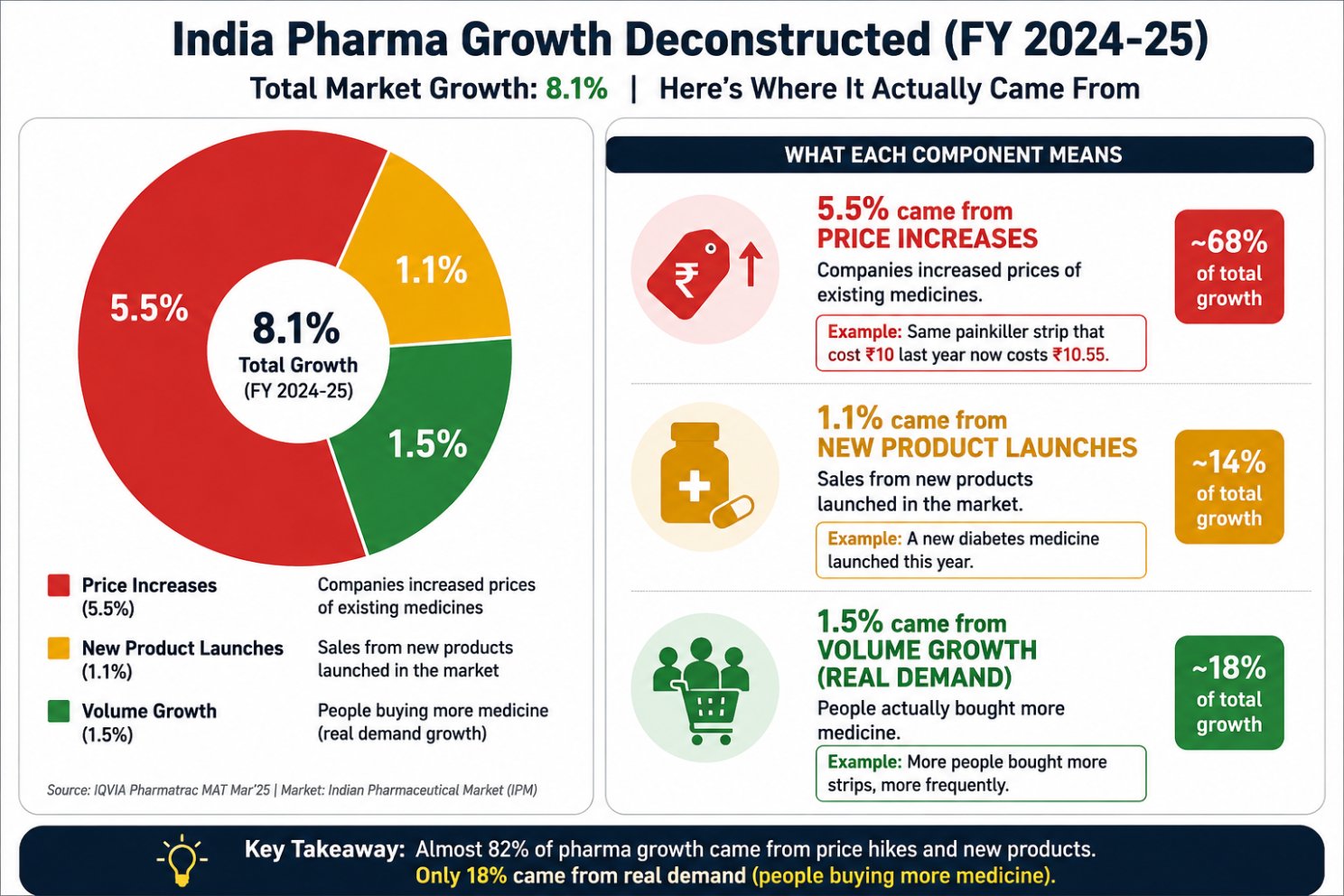

Decoding the 8.1% growth story

India's pharmaceutical market grew 8.1% in 2025 to reach ₹2,40,672 crore (Pharmarack MAT Dec 2025). That number gets celebrated in every quarterly call, every analyst report, every government press release. But break it open and a darker story falls out.

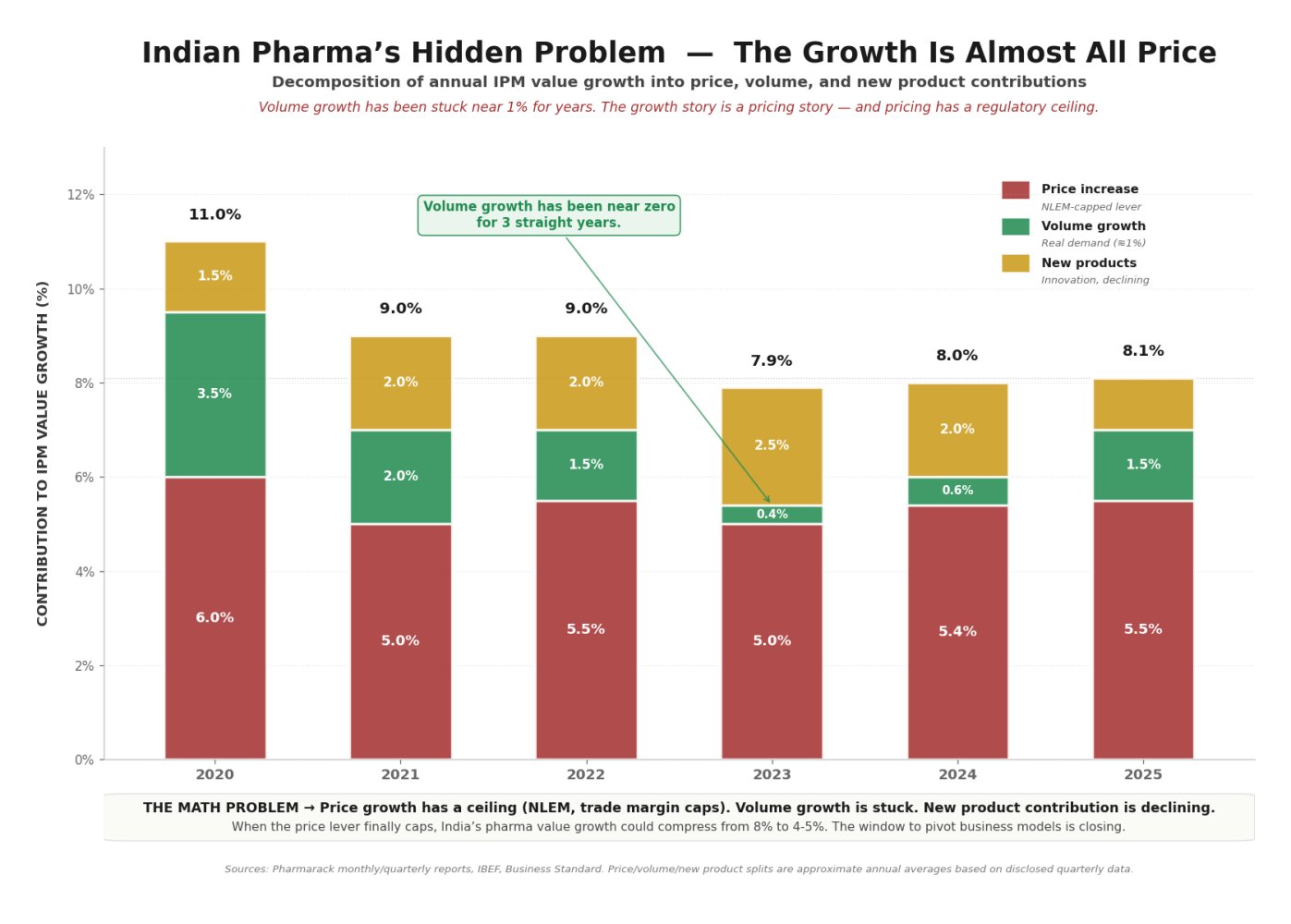

This isn't a one-year blip. Volume growth has been near 1% for three straight years: 0.4% in 2023, 0.6% in 2024, 1.5% in 2025. Indians are not buying meaningfully more medicine each year. Companies are just charging more for what people already buy. This is the most important fact about Indian pharma in 2025, and almost no industry report leads with it.

If volumes don't grow and prices can't keep rising, the entire industry's growth could compress from 8% to 4–5% within 3–5 years. For a ₹2.4 lakh crore industry, that's a ₹10,000+ crore problem.

Why this math is a slow-moving crisis

Raising prices works until it doesn't. Three forces are closing the window. First, price controls are expanding: the National List of Essential Medicines (NLEM) caps how much companies can charge on a growing list of drugs. Second, generics keep eroding margins: when a drug goes off-patent, multiple companies launch the same molecule and prices collapse within months. Third, trade margins are under regulatory scrutiny: what pharmacies and distributors earn is being capped.

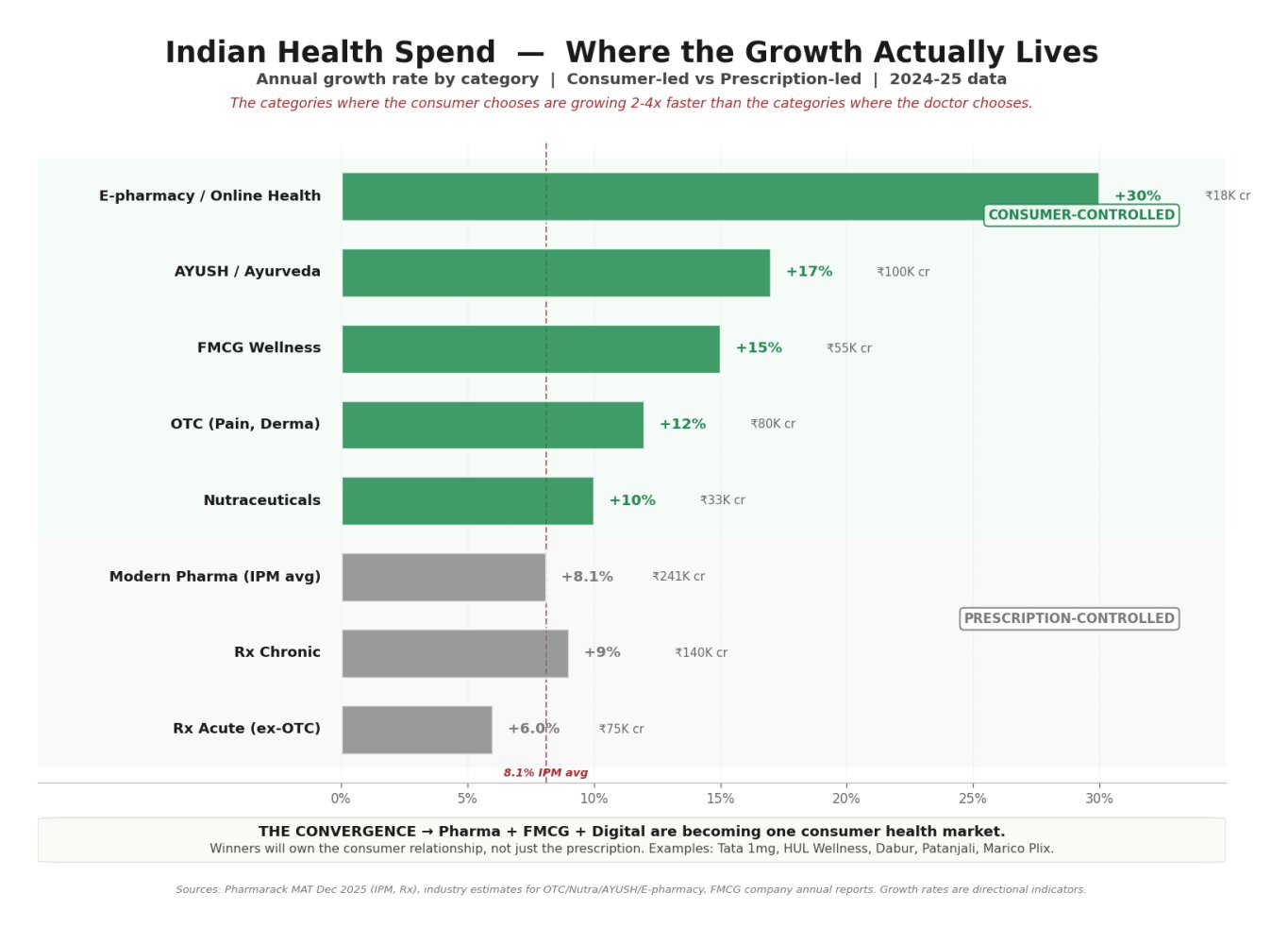

The consumer is quietly escaping the prescription system

While CEOs negotiate the next price increase, something fundamental is shifting in how Indians actually buy healthcare.

E-pharmacy apps (Tata 1mg, PharmEasy, Truemeds) are growing ~30%. AYUSH and Ayurveda ~17%. FMCG wellness ~15%. OTC categories ~12%. Nutraceuticals ~10%. Compare that to prescription pharma at 6–9%. The categories where the consumer chooses are growing 2–4x faster than where the doctor prescribes. That is not a trend, it's a structural shift, and it's happening while pharma boardrooms still optimize the prescription playbook.

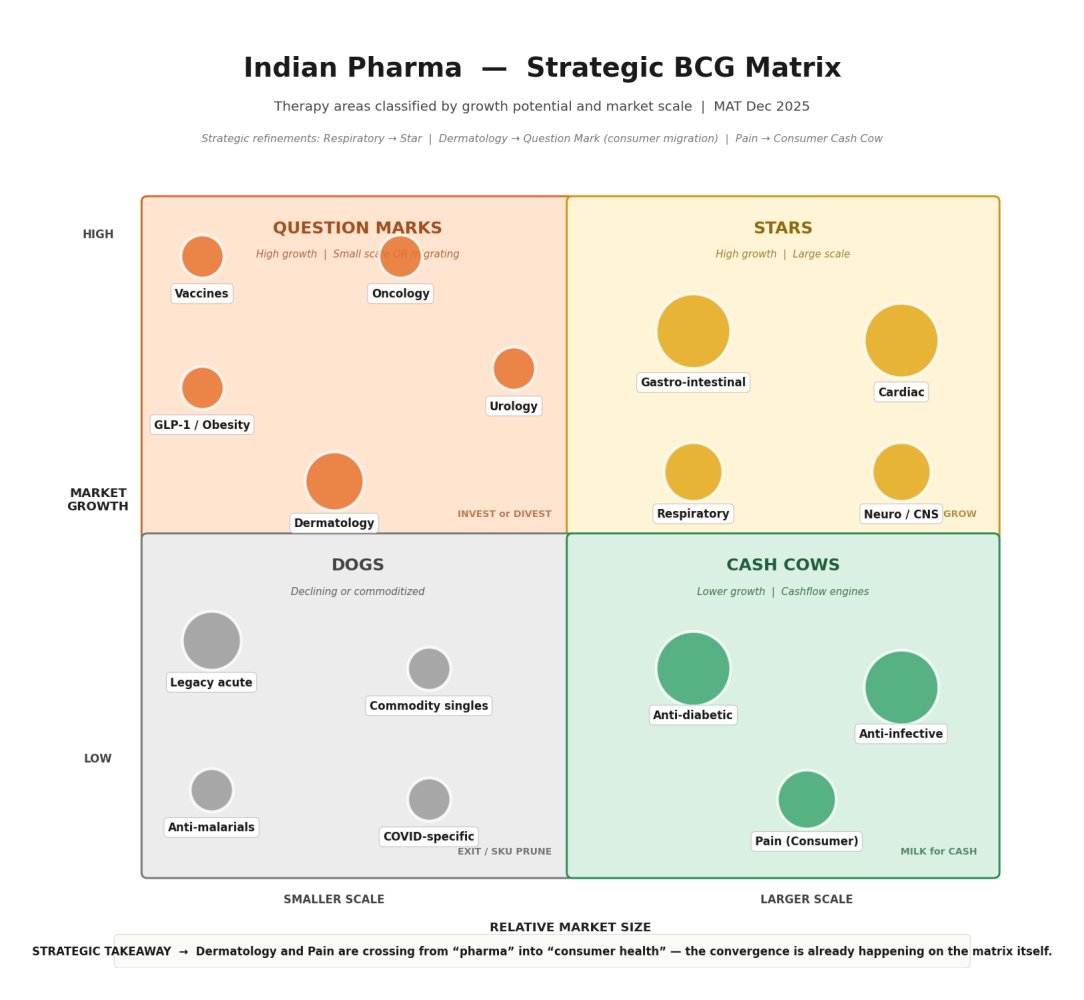

The strategic map is already showing the shift

Two therapy areas are visibly migrating. Dermatology (₹14,500 cr) is moving from prescription pharma to consumer and D2C, with acne products, anti-fungals, hair-loss treatments and pigmentation creams increasingly bought through Nykaa, Plix, Mamaearth and the Instagram economy. Pain/analgesics (₹14,000 cr) is already an FMCG category: Crocin, Combiflam and Volini are bought like soap, not prescriptions. And in the Question Marks quadrant, GLP-1 obesity drugs are the new wildcard, with Mounjaro marketed to consumers, not doctors.

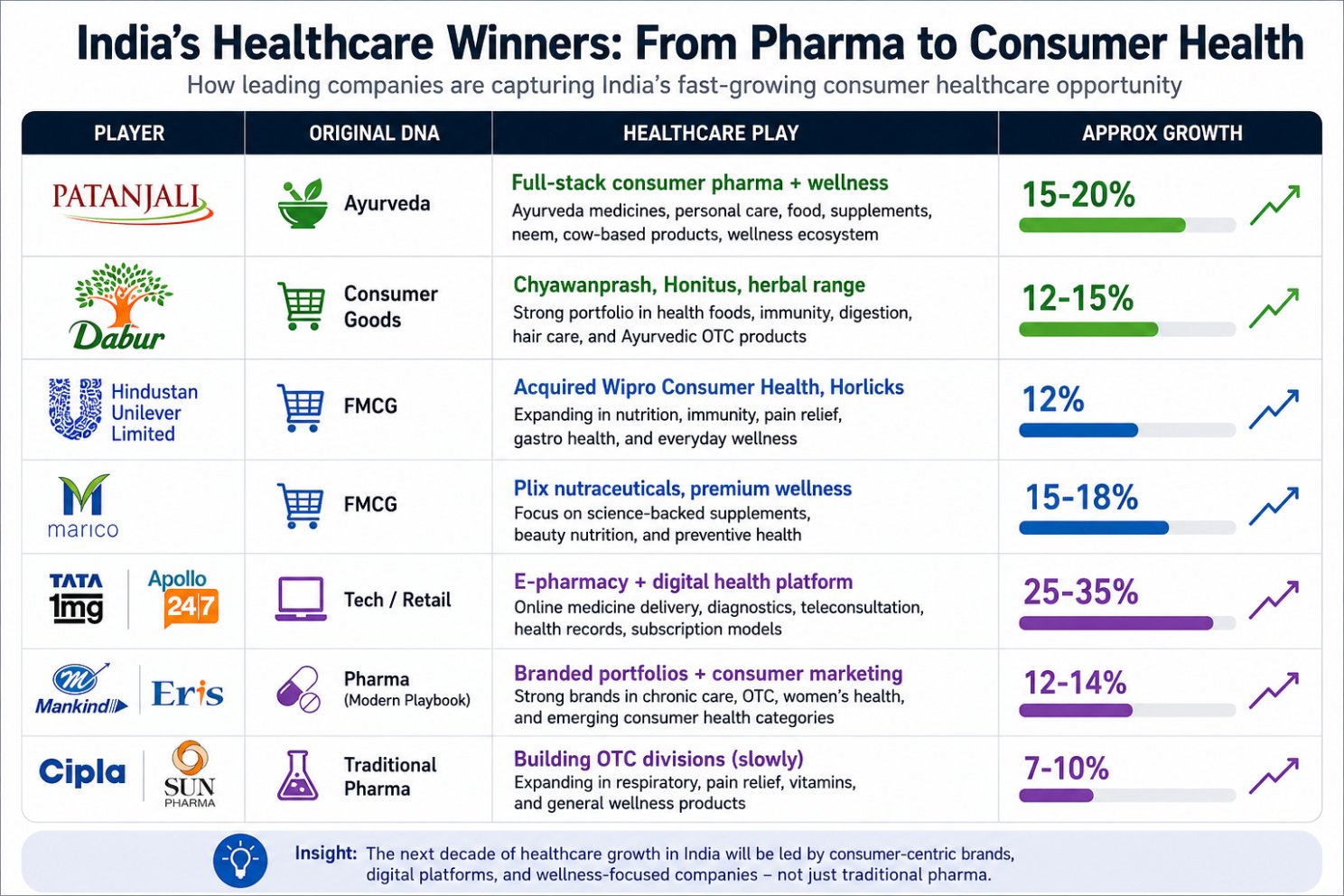

Who is already winning

The companies winning the next decade are not the ones with the best drug molecules. They're the ones building consumer brands in healthcare. The top players (Patanjali, Dabur, HUL, Marico, Tata 1mg, Apollo, Mankind/Eris) are growing 12–35% annually. The traditional pharma giants are stuck at 7–10%. The next ₹50,000 crore healthcare company most likely won't come from the traditional pharma side.

The real question

If 60–70% of incremental Indian healthcare spend over the next five years flows through non-prescription channels — OTC, nutraceuticals, AYUSH, FMCG wellness, e-pharmacy — what business is "pharma" actually in? The honest answer: the industry is converging with consumer FMCG, and most boardrooms are still running the old playbook of detailing doctors and defending molecules.

What this means for you

If you're a pharma CEO

Defend Cardiac, Anti-diabetic and CNS aggressively, but build a consumer health franchise alongside, in the next 2–3 years, not 10.

If you're an investor

Look beyond Sun, Cipla, Dr Reddy's. The next decade's alpha may live in Dabur, Marico, ITC, Apollo HealthCo and the e-pharmacy stack.

If you're a founder

The white space isn't another generics platform. It's the chronic-care consumer stack: drug + diagnostic + adherence + delivery + wellness.

If you're a policymaker

The boundary between "pharma" and "FMCG" is dissolving. Regulation, taxation and quality controls need to reflect this new reality.

The next "Cipla of India" won't be a pharma company. It will be a consumer health platform that happens to sell some prescription drugs alongside its supplements, devices, diagnostics and digital services.

Forty years ago, "is this pharma or FMCG?" was simple. A Crocin tablet was pharma; a jar of Horlicks was FMCG. Today Crocin is bought without prescription, Horlicks makes pharma-regulated health claims, and Patanjali, Apollo and Tata sell both. The categories have already merged. The companies are just slower to admit it. The 1% problem isn't really about volume. It's about identity.